Introduction

The microfinance and non-financial financial institutions (NFIs) industry in India caters to millions of people excluded from mainstream financial services. These are small businesses in Tier 2 and Tier 3 cities, daily wage earners, women-led self-help groups and first-generation entrepreneurs, who rely on timely access to credit for sustaining their livelihood.

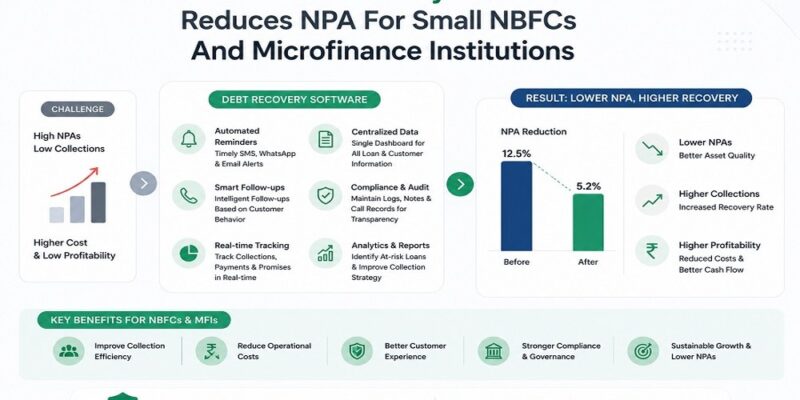

But lending at this scale comes with a real challenge – collections. When repayments slip, NPAs (Non-Performing Assets) climb, and for smaller institutions operating on thin margins, even a modest rise in NPA can strain liquidity fast. This is precisely where debt recovery software has started making a measurable difference.

The Ground Reality of NPA in Small NBFCs and MFIs

Increased NPAs in the NBFC-MFI sector have been a matter of concern for the Reserve Bank of India (RBI) for quite some time. Smaller banks have concentrated risk, while larger banks can withstand shocks by diversifying their portfolio. One geography or one segment of borrowers can quickly become problematic if there are a number of defaults.

Traditionally, collections were done using field agents, manual follow-up registers, and telephone calls, which are inconsistent and difficult to scale. There were no followups, and poor visibility of escalation was shared with recovery teams and there was no data integration.Recovery teams were always reactive, not proactive, as a result of missed followups, lack of visibility of escalation and no data integration.

Where Debt Recovery Software Changes the Game

1. Early Delinquency Detection

Good debt recovery software doesn’t wait for a loan to become an NPA. It flags accounts moving into early delinquency – at DPD 1 or DPD 7 – so recovery teams can act while the borrower relationship is still intact. In microfinance, early intervention is often the difference between a one-time missed EMI and a full write-off.

2. Automated Follow-Up Workflows

The software reminds users to make follow-up calls on their own without relying on an agent to remember, such as with SMS reminders in local languages, IVR calls, and WhatsApp nudges. A reminder in Marathi or Odia in a rural Maharashtra or Odisha is not the same as a standard English reminder.

3. Field Agent Efficiency

Debt recovery software with mobile-compatible field modules allows agents to update visit outcomes in real time, capture geo-tagged proof of visit, and receive priority account lists each morning. This cuts down idle time significantly and ensures no account falls through the cracks because of communication gaps between field and back office.

4. Portfolio Segmentation and Risk Prioritisation

Treatment of overdue accounts should not be the same for all. If a borrower has not been able to make a single EMI due to a family wedding, he is not the same person as a borrower who has not been able to make EMIs for 60 days. With software segmentation, recovery managers can focus on high-risk accounts and the most appropriate intervention – call, field visit, legal notice – according to real data, and not on the basis of a guess.

5. Legal and Regulatory Compliance Tracking

The lending laws pertaining to collections have become more stringent in India. There are RBI guidelines for the protection of NBFC and MFI borrowers. Debt recovery software records each interaction, keeps track of your communications, and ensures your collection efforts remain within the parameters – which means you’ll be less likely to face regulations fines or borrower complaints.

The Real Impact on NPA Reduction

Institutions that have moved from manual processes to structured debt recovery software have reported meaningful improvements in collection efficiency, reduced roll-forward rates between buckets, and better recovery on written-off portfolios. The compounding effect of catching early delinquency, improving agent productivity, and maintaining compliance adds up – and for a small NBFC, even a 1-2% reduction in gross NPA translates directly into improved capital adequacy and credit ratings.

Conclusion

Management of NPAs is no back office issue for small NBFCs and microfinance institutions in India, it’s a survival priority. Previously, a debt recovery process was human-centric, disjointed, and slow, but with the introduction of debt recovery software, it has become structured, faster, and more intelligent. With the competition getting tougher and regulators growing more exacting, the right investment in the right recovery infrastructure now will be a real advantage tomorrow.

Comments